In my role with the North Dakota Small Business Development Centers (NDSBDC), I have the privilege of working every day with founders of ND small businesses in our region. A common question I hear is, “How can I assess the performance of my business?” My answer is, “Start by looking at your financial statements.”

But what role does each of these financial statements play? How are they related? And how can you interpret and use the data to make better financial, investment and management decisions for your business? Let’s start with an overview of the three basic financial statements.

The Income Statement

Think of the income statement as a performance report card. It’s a useful tool for providing an overview of how your business is performing over time. It breaks down revenue or income generated, direct and fixed expenses incurred and profitability over a period of time.

Many small business owners are quick to refer to their income statement (or profit and loss statement), and that’s a good starting point. However, the P&L can provide only limited perspective. To have a more holistic view of the business, one needs to consider the other two basic financial statements: the balance sheet and cash flow statement. Together, these three basic financial statements can provide a more complete view of an organization’s financial situation.

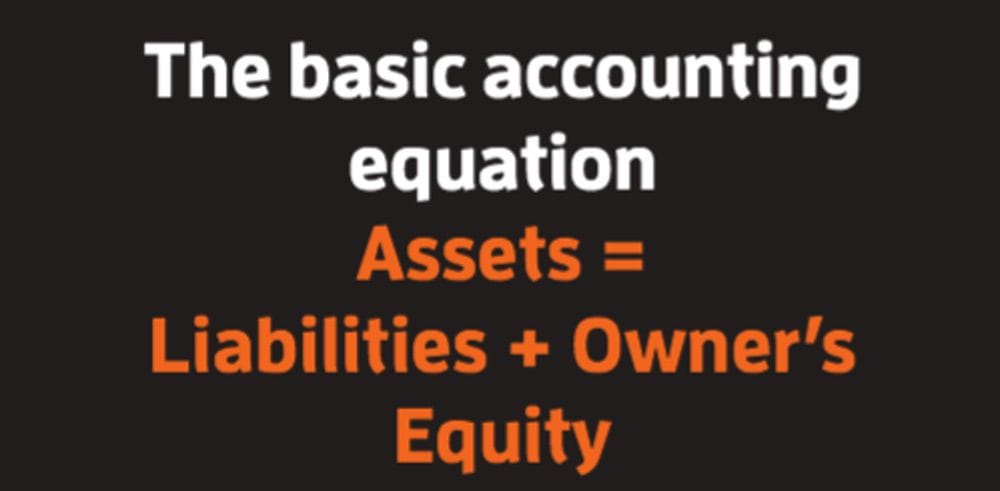

The Balance Sheet

Think of the balance sheet as a window into your business’s financial strength. Unlike the income statement, the balance sheet summarizes key financial information on a given date. It lists your business assets (what you own), liabilities (what you owe) and owner equity (what’s left over for the owners) or the “book value” of the business. It’s a good indicator of company stability and liquidity, which are both important factors in determining your business’s ability to sustain itself without outside financing.

The Cash Flow Statement

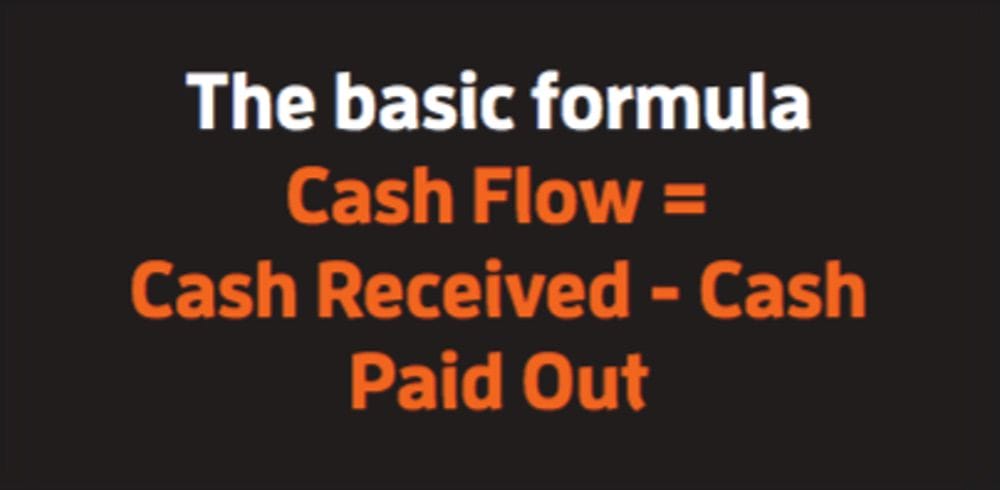

The cash flow statement is the often neglected but critical link between the income statement and balance sheet and answers the question, “Does your business have sufficient cash to stay afloat?” While the income statement shows business performance over a period of time, and the balance sheet tells you about your overall financial health at a particular point, the cash flow statement tells you how much money (from operations, investing and financing) is moving into and out of your business during a given month. If there is more cash in the bank at the end of the month than when you started, your business is cash flow positive. If you have less cash at the end of the month, your business had negative cash flow.

For example, if you received $15,000 in cash from your customers last month and paid out $10,000, your total cash flow would be $5,000.

More businesses fail because of cash flow issues than for any other reason. Your business can be profitable yet still have cash flow problems.

For example, I work with a client who owns a service business, which looks profitable on the P&L statement but has to wait 30-60 days to get paid by its customers. That money owed for services provided will be listed as accounts receivable on the balance sheet, and until a receivable has been paid and gets converted into cash, the money can’t be used to purchase more inventory, buy equipment or pay employees. That’s why it’s possible for companies to grow themselves right out of business. The faster a company grows, the more working capital is needed. Cash truly is the lifeblood of any business.

With a basic understanding of the three financial statements, we can do some basic financial statement analysis. The purpose is to identify patterns or trends over time and understand the relationship among the various accounts in order to make better operational, financial and investing decisions.

This analysis includes:

Internal trends analysis

Horizontal analysis – The actual or percentage change from the previous to current period.

Steps:

- Calculate change: Current – previous

- Divide by previous – Amount of change/previous

Examples:

- Income statement: Change in sales, COGS, gross profit margin, expenses, net income

- Balance sheet: Change in AR, inventory, AP, current liabilities, long-term debt, retained earnings

Vertical analysis – The percentage analysis of the relationship of each component in a financial statement to a total within a statement

For the balance sheet, the percentages are computed as follows:

- Each asset item is stated as a percent of total assets

- Each liability and stockholders’ equity item is stated as a percent of total liabilities and stockholders liabilities

- Component account/total = %

Example:

- Accounts receivable as % of total assets

For the income statement, each item is stated as a percent of sales

- Account/sales = %

- Example: Gross profit margin as % of sales

Financial ratios

Financial ratios are used to measure solvency, profitability, efficiency and risk in a business. Below are some common ratios, which can be calculated using numbers on the income statement and balance sheet.

Current ratio: Shows how many dollars in current assets for every dollar in current liabilities.

- CR = Current assets/current liabilities

Quick ratio: Similar to current ratio but includes only those assets that can be converted to cash immediately (excludes inventory and prepaids).

- QR = Quick assets/current liabilities

Working capital: Used to evaluate a company’s ability to pay its current liabilities.

- WC = Current assets/current liabilities

Accounts receivable turnover: Measures how frequently during the year the AR is being converted to cash.

- AR Turn = Sales/average AR

Inventory turnover: The relationship between the volume of goods sold and inventory.

- Inventory Turn = Cost of goods sold/average inventory

Sales to assets: Measures how effectively a company uses its assets.

- Sales to assets = Sales/total assets

Return on investment:

- Net profit (before tax)/net worth

Debt-to-worth: Represents a comparison of company financing provided by lender investors compared to financing provided by owner investors.

- Debt-to-worth = Total liabilities/net worth

As important as it is to spot trends, it can be even more important to forecast and budget future revenue, expenses and cash flow so you can anticipate when your business might need additional capital to fund seasonal fluctuations, purchase inventory to support sales growth or buy a new piece of equipment. You can then plan ahead and talk with your lender about obtaining a commercial loan or line of credit to ensure your business has sufficient cash when it needs it.

About Paul

Smith is Center Director of the ND Small Business Development Centers – Fargo. He was also named 2019 State Star for the organization. The ND SBDC assists each year more than 1,000 ND small business owners across the state to start, manage and grow their businesses. The SBDC provides free, confidential business advising, technical assistance and training in a wide range of areas. The Fargo Center is located in the NDSU Research and Technology Park Incubator. To register for services, visit their website: ndsbdc.org